A virtual dollar card is a digital payment card that lets you spend in US dollars online; without needing a physical card.

Think of it as your gateway to global payments.

Instead of relying on a local bank card that may fail on international platforms, a virtual dollar card gives you a USD balance and card details (number, expiry date, CVV) that work seamlessly across global websites.

How it works

- You sign up with a provider

- Verify your identity

- Fund your account in your local currency

- The platform converts it to USD

- You get a ready-to-use virtual card

From there, you can pay for anything from subscriptions to ads; just like a regular debit card.

Why it exists

Many local bank cards, especially in regions with foreign exchange controls, struggle with international payments.

A virtual dollar card solves that by:

- Operating in USD

- Bypassing local currency limitations

- Increasing payment success rates globally

Virtual Dollar Card Requirements in 2026

Getting started is easier than most people think, but there are still a few key requirements you must meet.

Basic Eligibility Criteria

To get approved, you typically need:

- To be at least 18 years old

- A valid email address and phone number

- Access to a smartphone or computer

- Residency in a supported country

Most providers are now expanding coverage across Africa, Asia, and Latin America.

KYC Verification Explained

KYC (Know Your Customer) is no longer optional, it’s mandatory in 2026.

Here’s what you’ll usually need:

- Government-issued ID (passport, national ID, or driver’s license)

- A selfie for facial verification

- Sometimes proof of address (utility bill or bank statement)

Verification can take anywhere from a few minutes to 24 hours, depending on the provider.

Why this matters:

Stricter verification reduces fraud and increases your card’s acceptance rate on platforms like Google Ads and ChatGPT subscriptions.

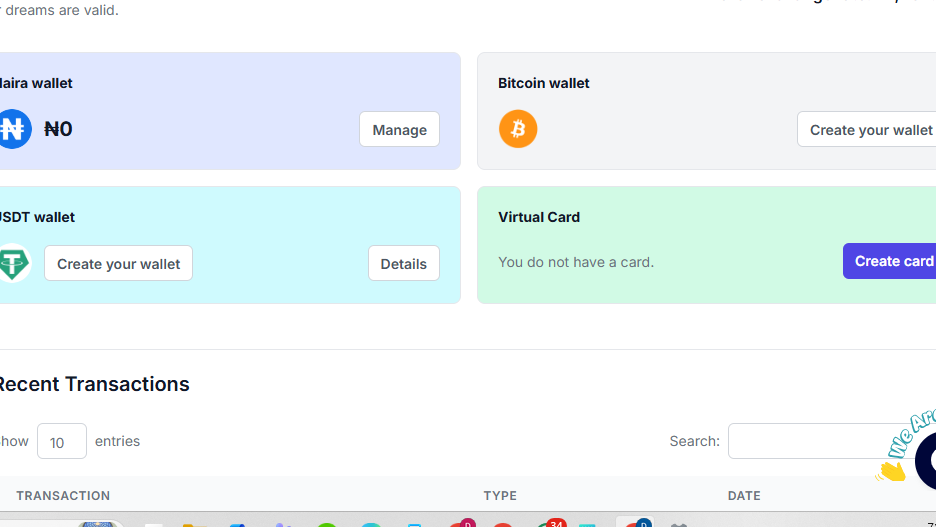

Funding Your Card

Once verified, the next step is adding money.

Common funding methods include:

- Bank transfer (local currency)

- Debit card funding

- Fintech wallet transfers

- Crypto (on select platforms)

Your funds are then converted into USD at the provider’s exchange rate.

Pro tip: Always check the FX rate and hidden fees before funding. This is where many users lose money without realizing it.

Step-by-Step: How to Get a Virtual Dollar Card

If you’ve never done this before, don’t worry, it’s a straightforward process.

Step 1: Choose a Trusted Provider

Not all providers are equal.

Look for:

- High success rate on international payments

- Transparent fees

- Strong user reviews

- Fast card issuance

A good provider should feel like a reliable financial tool, not a gamble.

Step 2: Sign Up and Verify

Create your account and complete KYC.

Make sure:

- Your details match your ID exactly

- Your selfie is clear and well-lit

Mistakes here can delay approval.

Step 3: Fund Your Card

Deposit funds using your preferred method.

At this stage:

- Check conversion rates

- Avoid funding small amounts repeatedly (fees add up)

Step 4: Start Paying Online

Once funded, your card is ready.

You’ll receive:

- Card number

- Expiry date

- CVV

Use these details just like a regular card on any supported platform.

Best Use Cases for Virtual Dollar Cards

This is where things get interesting.

A virtual dollar card isn’t just a workaround, it’s a powerful tool for global access.

1. Paying for Subscriptions

Many users rely on these cards for services like:

- Netflix

- Spotify

- Apple subscriptions

Local cards often fail here due to currency restrictions. A USD card removes that barrier.

2. Running Online Ads

If you run ads, you already know the struggle.

Platforms like:

- Facebook Ads

- Google Ads

…require reliable international payment methods.

A virtual dollar card improves:

- Payment approval rates

- Account stability

- Campaign continuity

3. Paying for SaaS Tools

From AI tools to hosting platforms, most SaaS products bill in USD.

Examples include:

- ChatGPT

- Design tools

- Developer platforms

Without a working USD card, access becomes difficult, or impossible.

4. Shopping on Global Websites

E-commerce platforms like:

- Amazon

- AliExpress

…work seamlessly with virtual dollar cards.

This is especially useful when:

- Your local card gets declined

- You want predictable USD pricing

Why Your Card Gets Declined (And How to Fix It)

Here’s the truth: even the best card can fail if something is off.

Let’s break down the most common issues.

1. Billing Address Mismatch

If your billing details don’t match what the platform expects, your payment may fail.

Fix:

Always use the billing address linked to your card provider.

2. Insufficient Funds

Seems obvious, but it’s a top reason for failed payments.

Remember:

- Some platforms add temporary charges

- FX fluctuations can affect balance

Fix:

Keep a small buffer above the required amount.

3. Platform Restrictions

Some platforms block certain card issuers or regions.

Fix:

Switch providers or try another payment method.

4. Suspicious Activity Flags

Rapid transactions or unusual patterns can trigger security blocks.

Fix:

- Avoid repeated failed attempts

- Contact your provider if needed

Virtual Dollar Card vs Local Bank Cards vs Crypto Cards

To really understand the value of a virtual dollar card, you need to see how it compares with other payment methods people still rely on.

Key Differences

| Feature | Virtual Dollar Card | Local Bank Card | Crypto Card |

|---|---|---|---|

| Currency | USD | Local currency | Crypto converted |

| Global acceptance | High | Often limited | Mixed |

| FX stability | Stable (USD-based) | Unstable | Volatile |

| Setup speed | Fast | Slow | Medium |

| Online subscriptions | Works reliably | Often fails | Depends on platform |

What this means in real life

- If you’re paying for subscriptions, SaaS tools, or ads → virtual dollar card is the most reliable option

- You’re staying local → bank card is fine

- You’re deep in Web3 → crypto cards can work, but they’re inconsistent for mainstream platforms

For most users today, the virtual dollar card has become the “default global payment key.”

Virtual Dollar Card Providers Compared

Not all providers are built the same. In fact, your experience depends heavily on which one you choose.

What a good provider must offer in 2026

A reliable provider should give you:

- Fast onboarding and approval

- Stable USD funding and conversion

- High success rate on global platforms

- Transparent fees (no hidden FX surprises)

- Strong identity verification (KYC compliance)

If a provider fails in any of these areas, you’ll feel it immediately when payments start declining.

What users actually care about (real-world insight)

From user discussions across fintech communities and forums, the priorities are simple:

- “Does it work on Netflix without failing?”

- “Can I run ads on Facebook Ads smoothly?”

- “Will my card get blocked after a few transactions?”

These are the real benchmarks; not marketing claims.

Current 2026 Regulations and Payment Limits

The global payments landscape in 2026 is stricter than ever, especially for cross-border transactions.

FX pressure and local restrictions

In countries like Nigeria, users still face:

- Limited access to USD through traditional banks

- Spending caps on international transactions

- Frequent declines on foreign platforms

This is why virtual dollar cards have become essential infrastructure for digital workers and online businesses.

Compliance and verification trends

Most providers now enforce:

- Tiered KYC levels (basic → advanced verification)

- Spending limits based on identity verification

- Enhanced fraud monitoring systems

This isn’t optional, it’s part of global financial regulation alignment.

Security Tips You Should Not Ignore

A virtual dollar card is powerful, but only if used responsibly.

Protect your card like a bank asset

- Never share your card details publicly

- Avoid saving card info on untrusted websites

- Use only verified platforms for payments

Watch for payment red flags

Be cautious if you notice:

- Repeated payment failures on the same platform

- Unexpected declines despite sufficient funds

- Requests for unusual verification steps

These often signal either provider issues or platform restrictions.

Pros and Cons of a Virtual Dollar Card

Before choosing any provider, it’s important to understand the trade-offs clearly.

Advantages

- Works globally across USD-based platforms

- Solves local currency and FX limitations

- Fast setup and activation

- Ideal for subscriptions, SaaS, and ads

- Reduces payment friction significantly

Limitations

- FX conversion fees may apply

- Some platforms still block certain issuers

- Spending limits depend on verification level

- Requires KYC documentation

Final Verdict: Is a Virtual Dollar Card Worth It in 2026?

Yes, especially if you operate in the global digital economy.

A virtual dollar card is no longer a “nice-to-have.” It has become a core financial access tool for:

- Freelancers earning globally

- Digital marketers running ad campaigns

- Developers paying for SaaS tools

- Creators managing subscriptions and online services

But the real challenge is not just getting a card; it’s choosing the right ecosystem that keeps your payments stable, compliant, and friction-free.

Smarter Way to Manage Your Global Payments

Here’s the truth most users discover too late:

Having a virtual dollar card is only half the solution.

Managing it properly; tracking spending, avoiding declines, choosing the right funding method—is where real efficiency comes in.

That’s where EverTry comes in.

EverTry is built to simplify global payments for users who constantly deal with USD subscriptions, ads, and international platforms. Instead of juggling multiple failed cards or confusing providers, EverTry helps you:

- Access and manage virtual dollar payment options in one place

- Reduce failed transactions on global platforms

- Track spending and FX conversions more clearly

- Stay in control of your digital financial activity

If you’ve ever struggled with payment failures, blocked subscriptions, or confusing card providers, EverTry is designed to remove that friction entirely.

Take Control of Your Global Payments

Instead of guessing which virtual dollar card works, you can simplify everything in one step.

Your access to the global digital economy shouldn’t be complicated, and with EverTry, it isn’t.

Download EverTry on iOS and Android today.

This article is for informational purposes only and does not constitute financial or legal advice. Virtual dollar card features, requirements, and availability may change, so users should verify details with their provider. EverTry is not responsible for any third-party services, transaction issues, or financial losses.

Deborah Giwa is a Marketing Associate at EverTry, where she works on content and growth initiatives focused on helping users navigate international payments. She is passionate about simplifying access to global financial tools for people in emerging markets through clear, practical, and user-focused content.