DeepSeek Chat is free, but DeepSeek API usage requires payment in US dollars. DeepSeek accepts Visa, Mastercard, PayPal, Alipay, and WeChat Pay, but many African bank cards are declined at checkout because of foreign exchange restrictions and international spending limits set by local banks and central banks. The most reliable solution is a virtual dollar card funded with your local currency or stablecoins, which lets you top up your DeepSeek account in minutes.

This guide explains exactly why your card fails, what works instead, and what the rules look like in 14+ African markets, from Lagos to Nairobi, Cairo to Dakar.

First, Check If You Actually Need to Pay for DeepSeek

Not every DeepSeek user needs to pay. DeepSeek Chat is free. The DeepSeek API is what costs money, and it’s billed based on how much you use it.

A lot of the “how do I pay for DeepSeek” frustration in African dev communities comes from people who never needed to pay in the first place. So before you go hunting for a card that works, check which side of DeepSeek you’re actually on.

Is DeepSeek Chat Free?

Yes. The consumer chat app at chat.deepseek.com (and the mobile app) is completely free. There is no Plus plan, no Pro subscription, and no paywall. If you’re using DeepSeek the way most people use ChatGPT, asking questions, drafting content, debugging code in the chat window, you don’t need to pay anything, and nothing in this guide applies to you yet.

When Do You Need to Pay?

You need a funded account when you move to the DeepSeek API at platform.deepseek.com. That means:

- Calling DeepSeek models from your own application or backend

- Building AI agents or automation workflows

- Running DeepSeek inside tools like coding assistants and pipelines

- Deploying DeepSeek for a team or product at scale

The API is prepaid: you top up a USD balance, and usage is deducted per token. There’s no monthly subscription and no minimum spend commitment.

DeepSeek’s Free Credits for Developers

New developer accounts receive a free grant of around 5 million tokens, no credit card required. That’s enough for thousands of test calls, so you can validate your integration before spending a single dollar. Once the grant runs out, you switch to pay-as-you-go.

DeepSeek Pricing Explained (and Why $10 Goes Far)

As of June 2026, DeepSeek’s lineup centres on two V4 models:

| Model | Input (per 1M tokens) | Output (per 1M tokens) | Best for |

|---|---|---|---|

| DeepSeek V4 Flash | $0.14 | $0.28 | Production workloads, high volume |

| DeepSeek V4 Pro | $1.74 | $3.48 | Flagship reasoning, complex coding |

Cache hits cost a fraction of standard input, and both models ship with a 1M-token context window. Always confirm current rates on DeepSeek’s official pricing page before budgeting; they change.

Here’s the practical math: one million tokens is roughly 750,000 English words. At V4 Flash rates, a $10 DeepSeek balance can power millions of AI-generated words before you need another top-up. For a freelancer in Accra or a two-person startup in Kampala, a single small top-up can run a side project for months.

That’s exactly why the payment problem is so frustrating. The service costs almost nothing. Getting $10 across the border is the hard part.

What Payment Methods Does DeepSeek Accept?

DeepSeek currently accepts Visa, Mastercard, PayPal, Alipay, and WeChat Pay for account top-ups, according to its official billing FAQ. One detail worth knowing: your topped-up balance never expires, so there’s no risk in funding a little more than you need.

| Method | Accepted by DeepSeek | Practical for Africa? |

|---|---|---|

| Visa | Yes | Yes, if the card can transact internationally |

| Mastercard | Yes | Yes, same condition |

| PayPal | Yes | Country-dependent (see below) |

| Alipay | Yes | Rarely usable outside China |

| WeChat Pay | Yes | Rarely usable outside China |

| Crypto (direct) | No | — |

| Mobile money (direct) | No | — |

| Bank transfer (direct) | No | — |

Does DeepSeek Accept Crypto?

No, and this is the most common misconception on this topic. Several pages ranking for “buy DeepSeek” are actually about a speculative token, not the AI service. DeepSeek does not accept cryptocurrency at checkout. Stablecoins only work when used to fund a card or wallet that then pays DeepSeek in USD. If you hold USDT or USDC, you’re one step away from paying, but the step is a card, not a wallet address.

Does DeepSeek Accept Mobile Money?

Not directly. M-Pesa, MTN MoMo, Airtel Money, and Wave can’t talk to DeepSeek’s checkout. But they matter enormously as the funding rail: in most African countries, mobile money is the fastest way to load a virtual dollar card, which then completes the payment.

Does DeepSeek Accept Bank Transfers?

No. There’s no IBAN or wire option for individual top-ups. Like mobile money, your bank account’s role is upstream; it funds whatever card you use at checkout.

Why Your Local African Card Gets Declined on DeepSeek

Most DeepSeek payment failures in Africa happen for one of three reasons: foreign exchange restrictions, issuer-side international spending limits, or payment gateway compatibility. Your bank balance is usually not the problem.

Understanding FX Controls

DeepSeek bills in US dollars. When you pay with a naira, cedi, or kwacha card, your bank has to source dollars to settle that transaction. In countries where central banks are defending thin foreign reserves- Nigeria for much of 2022–2025, Egypt since 2022, and Malawi chronically- banks are told (or choose) to restrict how many dollars flow out through retail cards. The decline message you see is the last link in that chain.

International Spending Limits

Even where international payments are allowed, they’re capped. Nigerian banks reinstated international use of naira cards in mid-2025 with quarterly limits useful, but a $1,000/quarter cap disappears fast once Netflix, Apple, Google Ads, and your AI tools are all drawing from it. Egyptian banks require some customers to pre-authorise foreign-currency spending entirely.

Currency Conversion Challenges

Where FX is scarce, banks also worry about settlement, actually delivering dollars to Visa and Mastercard. Some respond by silently declining foreign-merchant transactions even within official limits. This is why a card that worked last month can fail this month with nothing changed on your end.

Payment Gateway Compatibility

DeepSeek is a Chinese company, and its card processing has a different risk profile than, say, Netflix’s. Some African-issued cards face elevated decline rates on less familiar international gateways regardless of FX rules; the issuer’s fraud model simply scores the merchant as risky and blocks it.

Why Having Money in Your Account Isn’t Enough

The problem is often not your bank balance. It is your currency’s access to dollars.

A card can be declined with six figures of local currency sitting behind it. Once you understand that the bottleneck is currency access, not creditworthiness, not funds, the fix becomes obvious: pay with a card that’s already denominated in dollars, so the conversion happens before checkout, not during it.

Best Ways to Pay for DeepSeek AI in Africa

Across the continent, three methods consistently work. Virtual dollar cards are the most reliable option in every market covered in this guide, followed by PayPal (in a handful of countries) and stablecoin-funded cards.

Method #1: Virtual Dollar Cards (Recommended)

A virtual dollar card is a USD-denominated Visa or Mastercard issued instantly inside a fintech app. You fund it in your local currency or stablecoins; the app converts to dollars at funding time; DeepSeek’s checkout sees a clean US-dollar card.

Why it works: because the card is already in USD, it sidesteps your bank’s FX card limits entirely. There’s no naira-to-dollar conversion happening at the moment of payment, which is exactly the moment local cards fail.

Several providers issue virtual dollar cards across Africa, including EverTry, which supports funding in 14 African currencies plus USDT and USDC. Whichever provider you use, the mechanics below are the same.

Pros

- Accepted anywhere Visa/Mastercard is accepted, including DeepSeek

- Setup typically takes under 15 minutes

- Built-in budget control, you can fund exactly what you plan to spend

Cons

- Requires funding the card first (one extra step vs. a bank card)

- Card creation and FX fees vary by provider — compare before committing

Works in: Nigeria, Ghana, Kenya, Egypt, Cameroon, Senegal, Côte d’Ivoire, Zambia, Uganda, Tanzania, Rwanda, Malawi, Botswana, South Africa, and most other African markets.

Method #2: PayPal

DeepSeek accepts PayPal, but PayPal does not treat African countries equally.

Where it works well: Kenya, South Africa, and Botswana have full send-capable PayPal accounts. If you already keep a funded PayPal balance there, it’s a perfectly good way to pay.

Where it doesn’t: Nigerian PayPal accounts have historically been receive-restricted or limited for merchant payments, and Cameroon and several other markets face similar constraints. If your PayPal account can’t make purchases, no amount of funding will fix the DeepSeek checkout.

| PayPal | |

|---|---|

| Setup time | Fast if you already have an account |

| Coverage | A minority of African countries |

| Fees | FX conversion spread on non-USD balances |

| Verdict | Good where available; not a pan-African answer |

Method #3: Stablecoin-Funded Cards

If you’re paid in USDT or USDC, common for African freelancers and remote workers, you can skip the banking system entirely: USDT/USDC → fund a virtual dollar card → pay DeepSeek.

The FX conversion happens when you fund the card, not during checkout.

Pros

- Works where banking rails are weakest or parallel exchange rates distort card pricing

- Often the fastest route from “holding value” to “holding spendable dollars.”

Cons

- One extra conversion step (and spread) compared to fiat funding

- You’re responsible for sending to the correct network and address

Remember: this is not “paying DeepSeek with crypto.” DeepSeek never sees the stablecoin. The card is the bridge.

Country-by-Country Guide to Paying for DeepSeek

The table below summarises the landscape. Detailed notes for each market follow, including the regulator behind each restriction, because understanding why your card fails is the difference between guessing and fixing.

| Country / Zone | Main challenge | Best funding rail | PayPal? |

|---|---|---|---|

| Nigeria (NGN) | Quarterly international card limits; intermittent reliability | NGN bank transfer | Restricted |

| Kenya (KES) | FX markups, gateway declines | M-Pesa | Yes |

| Ghana (GHS) | Bank caps on foreign card spend | MTN MoMo / Telecel Cash | Limited |

| Egypt (EGP) | FX restrictions on cards since 2023 | InstaPay / bank transfer / USDT | Limited |

| South Africa (ZAR) | Cost, not access — FX markups | ZAR bank transfer | Yes |

| Botswana (BWP) | Merchant-side declines | BWP transfer | Yes |

| Malawi (MWK) | Chronic forex shortage | Airtel Money / TNM Mpamba / USDT | No |

| Zambia (ZMW) | Kwacha volatility, conservative banks | Mobile money / bank transfer | Limited |

| Tanzania (TZS) | Intermittent card enablement | M-Pesa / Tigo Pesa | Limited |

| Rwanda (RWF) | Cards disabled for international use by default | MTN MoMo | Limited |

| Uganda (UGX) | Low card enablement, markups | MTN MoMo / Airtel Money | Limited |

| XOF zone (8 countries) | Domestic-only card networks | Wave / Orange Money | Limited |

| XAF zone (6 countries) | BEAC FX regulation, strictest in the region | MTN MoMo / Orange Money | Limited |

| Stablecoin users | No direct crypto checkout | USDT / USDC → card | — |

Nigeria (NGN)

Nigerian naira cards may work on DeepSeek, but reliability is inconsistent and quarterly limits are tight. A virtual dollar card funded by NGN bank transfer is the dependable route.

Nigeria’s story explains the whole continent’s problem in miniature. Between 2022 and 2023, every tier-1 bank suspended international transactions on naira cards as dollar scarcity bit. For nearly three years, the “Do Not Honor” message became a rite of passage for any Nigerian developer trying to pay for foreign software.

In mid-2025, as FX liquidity improved under the CBN’s reforms, banks began re-enabling international use, with caps. GTBank reinstated a $1,000 quarterly limit (since raised substantially as dollar liquidity improved), First Bank capped standard cards around $500/month, and limits continue to vary by bank, by customer, and by quarter.

What this means in practice: your naira card might clear a $10 DeepSeek top-up today. But that quarterly allowance is shared with every other foreign payment you make, subscriptions, app stores, ad platforms, and banks adjust limits without much notice. For anything you depend on, fund a USD card via NGN transfer and remove the variable. If you keep a domiciliary account, that works too, but most developers find the branch-visit friction not worth it for small API top-ups.

Kenya (KES)

Kenya has no hard FX controls, so the challenge isn’t legality; it’s cost and reliability.

The Central Bank of Kenya runs one of Africa’s most liberal FX regimes; nothing stops a KES card from paying a foreign merchant. In practice, Kenyan cards carry FX markups of 3.5% or more, shilling volatility makes your USD costs drift month to month, and some issuers decline less familiar international gateways outright.

The Kenyan advantage is M-Pesa. The smoothest flow in the country is M-Pesa → fund a virtual USD card → top up DeepSeek — done from your phone in minutes, with the FX conversion locked at funding time instead of floating at checkout. Kenyan PayPal accounts also work on DeepSeek if you keep a funded balance.

Ghana (GHS)

Ghanaian banks cap or disable foreign online spending on many cedi cards; mobile money into a USD card is the path of least resistance.

Repeated cedi depreciation cycles have made the Bank of Ghana and commercial banks cautious about dollar outflows. Many GHS cards ship with low foreign e-commerce limits or have international spending disabled, and BoG’s broader stance against dollarization keeps the pressure on. Anyone in Accra who tracks “the dollar rate” daily already understands the dynamic.

Fund via MTN MoMo, Telecel Cash, or AT Money into a virtual dollar card, and your DeepSeek top-up is insulated from whatever the cedi does next quarter.

Egypt (EGP)

Egypt is the most restrictive card market in this guide. A USD virtual card isn’t a convenience here; it’s often the only consistent option.

In October 2023, amid a severe dollar shortage and a wide gap between official and parallel exchange rates, Egyptian banks suspended foreign-currency transactions on debit cards entirely, and the Central Bank of Egypt instructed banks to restrict and pre-authorise FX use on credit cards after observing speculative abuse. The March 2024 flotation and IMF deal eased the crisis, and some limits have loosened, but the architecture of restriction remains. Several banks still require documented travel plans before enabling meaningful foreign-currency card spending, and limits vary wildly by bank and card tier.

For an Egyptian developer, the workaround is structural: fund in EGP via Mobile Money (or USDT, which has deep liquidity in Egypt) into a USD card, and pay DeepSeek with a card that the CBE’s debit-card restrictions never touch.

South Africa (ZAR)

South African cards generally work on DeepSeek. The case for a virtual dollar card here is cost control, not access.

The South African Reserve Bank maintains exchange controls, but the single discretionary allowance, R1 million per person per year, is far more than anyone’s API bill. ZAR cards routinely clear international payments.

The friction is financial: banks charge roughly 2–2.75% FX markups, and a USD-billed API means your rand cost moves with the exchange rate. Teams budgeting AI spend in dollars often prefer to convert it once into a USD card balance and spend from there, locking the rate. If you have a funded South African PayPal account, that works too.

Botswana (BWP)

Botswana abolished exchange controls in 1999, pula cards usually work; declines are merchant-side quirks rather than policy.

Botswana runs one of the most open FX regimes in Africa. When a BWP card fails on DeepSeek, it’s typically the issuer’s fraud scoring of an unfamiliar gateway, not a regulation. A USD virtual card funded by Pula transfer solves the occasional decline and gives cleaner USD budgeting; PayPal is also fully functional.

Malawi (MWK)

Malawi’s chronic forex shortage means kwacha cards are routinely blocked or capped to trivial amounts for international use.

The Reserve Bank of Malawi devalued the kwacha 44% in November 2023, and dollar scarcity has remained a defining feature of the economy since, anyone who lived through the fuel queues knows it firsthand. Banks ration the FX they have, and retail card spending abroad sits at the bottom of the priority list.

For Malawian developers, the realistic flow is Airtel Money or TNM Mpamba → virtual USD card, or USDT funding if you’re paid in stablecoins. Direct MWK card payments to DeepSeek are best treated as unavailable.

Zambia (ZMW)

No hard capital controls, but kwacha volatility and conservative bank policies make ZMW cards unpredictable for foreign merchants.

The kwacha moves with copper prices, and Zambian banks respond to volatility by tightening card limits and declining riskier gateways. The Bank of Zambia has also pushed regulation reinforcing kwacha use domestically, keeping dollar access channelled. Fund a USD card via bank transfer, Airtel Money, or MTN MoMo, and the volatility becomes a one-time conversion decision instead of a recurring surprise.

Tanzania (TZS)

TZS cards work intermittently; low default e-commerce limits and policy direction favour the virtual card route.

Tanzania’s FX regime is liberalised, but the Bank of Tanzania’s 2025 regulations restricting domestic foreign-currency use signal where policy is heading, and many shilling cards carry low international e-commerce limits out of the box. M-Pesa (Vodacom), Tigo Pesa, or Airtel Money into a USD card is the dependable flow from Dar or Dodoma.

Rwanda (RWF)

Rwanda’s regime is open, but most RWF debit cards ship with international online payments disabled by default.

The National Bank of Rwanda doesn’t block foreign payments, your bank just probably hasn’t enabled them. Most local cards require a branch visit or a USSD request to unlock international e-commerce, usually with low caps. For Kigali’s fast-growing developer scene (Rwanda is actively positioning itself as an AI hub), MTN MoMo into a virtual USD card skips the enablement dance entirely.

Uganda (UGX)

Uganda has run a liberal FX regime since the 1990s; the barriers are practical, card enablement and markups, not legal.

Bank of Uganda policy permits foreign card spending freely, but many shilling cards aren’t internationally enabled, and those that are charge meaningful FX markups. MTN MoMo or Airtel Money → USD card → DeepSeek is the standard Kampala flow.

XOF Countries (Senegal, Côte d’Ivoire, Bénin, Togo, Mali, Burkina Faso, Niger, Guinea-Bissau)

Most domestic cards in the WAEMU zone can’t transact with foreign online merchants at all, the decline isn’t a limit, it’s a wall.

The BCEAO administers exchange controls for the eight-country West African franc zone. The CFA franc’s euro peg keeps the currency stable, but FX access runs through bank paperwork designed for trade, not for a developer’s $10 API top-up. Crucially, most cards issued on the regional GIM-UEMOA network are domestic-only: they simply aren’t built to talk to an international payment gateway. International Visa/Mastercard products exist but are unevenly issued and often restricted.

The good news: this is also the region with the best funding rails. Wave (the default in Senegal and Côte d’Ivoire) and Orange Money load a virtual dollar card in seconds. From Dakar or Abidjan, that two-step flow is faster than anything the banking system offers.

XAF Countries (Cameroon, Gabon, Congo-Brazzaville, Chad, CAR, Equatorial Guinea)

The CEMAC zone has the strictest FX regime in Sub-Saharan Africa. A USD virtual card funded by mobile money is effectively the standard workaround.

The BEAC’s 2019 foreign-exchange regulation requires banks to document and justify FX outflows, caps card spending abroad, and makes international card payments from the zone notoriously unreliable. Cameroonian developers, one of the most active and most underserved AI communities on the continent, feel this daily: capable engineers in Douala and Yaoundé locked out of $0.14-per-million-token APIs by settlement paperwork.

MTN MoMo and Orange Money are the rails. Fund a USD card with francs, and the BEAC documentation requirements stay between your card provider and its banking partners, not between you and your DeepSeek balance.

Paying with USDT or USDC

Stablecoins can’t pay DeepSeek directly, but they’re the most flexible funding source on the continent.

If you’re a freelancer invoiced in USDT, a developer paid by a foreign client, or anyone in a parallel-rate economy, stablecoins are probably already how you hold value. The flow is the same everywhere: send USDT or USDC to a virtual card provider, convert to card balance, pay DeepSeek. NGN/USDT is one of the deepest P2P currency pairs in the world, and liquidity in EGP, GHS, and KES pairs is strong, so moving between local cash and stablecoins is rarely the bottleneck. The card is.

Step-by-Step: How to Pay for DeepSeek with a Virtual Dollar Card

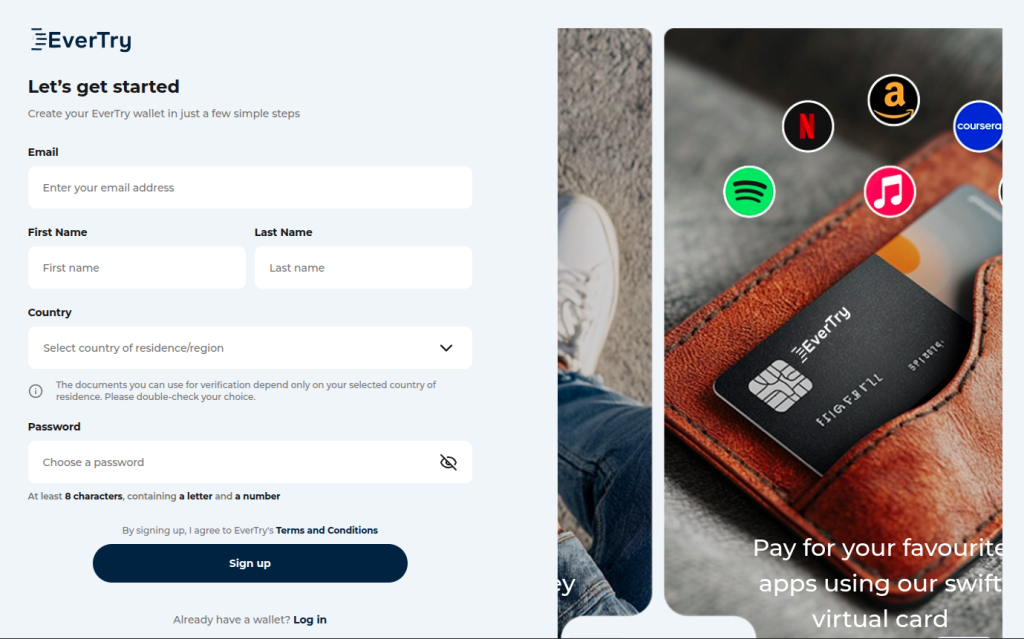

A virtual dollar card lets you fund your DeepSeek account in USD even when your local card can’t complete international transactions. Here’s the full flow using EverTry as the worked example, from a standing start, this takes under 15 minutes.

Step 1: Create and verify your account. Sign up and complete identity verification (a government ID and a selfie, in most cases). Verification on EverTry typically completes in minutes.

Step 2: Fund your wallet in your local currency or stablecoins. Supported funding options include NGN, KES, GHS, EGP, XOF, XAF, BWP, MWK, ZAR, TZS, RWF, ZMW, UGX, USDT, and USDC. Use whichever rail is native to you: bank transfer in Lagos, M-Pesa in Nairobi, MoMo in Accra, Wave in Dakar, USDT anywhere.

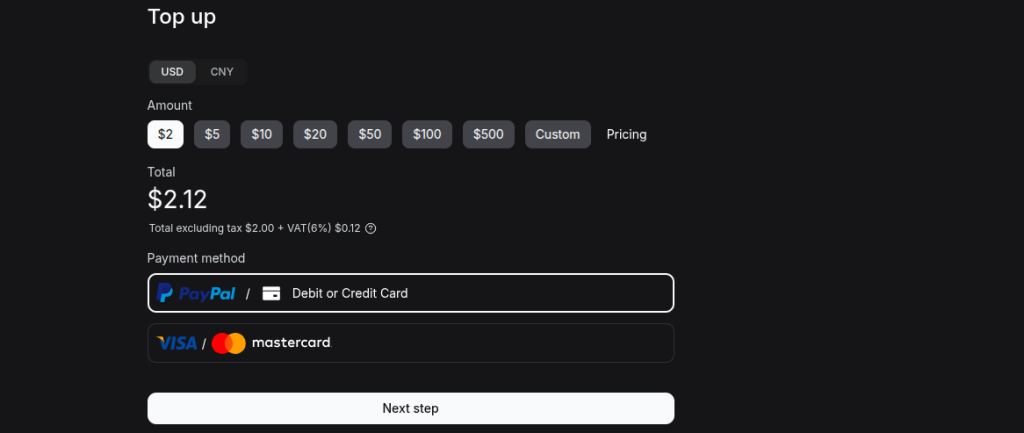

Step 3: Create your virtual dollar card. Convert wallet balance to USD and generate the card. You’ll get a card number, expiry, CVV, and a billing address. Fund it with $5–$10 to start; remember, DeepSeek balances never expire, so there’s no penalty for topping up a little extra.

Step 4: Go to the DeepSeek Platform. Visit platform.deepseek.com and log in (or create a developer account: you’ll get the free token grant on signup).

Step 5: Open Top Up. Select Top up from the left-hand menu, choose a preset amount or enter a custom one.

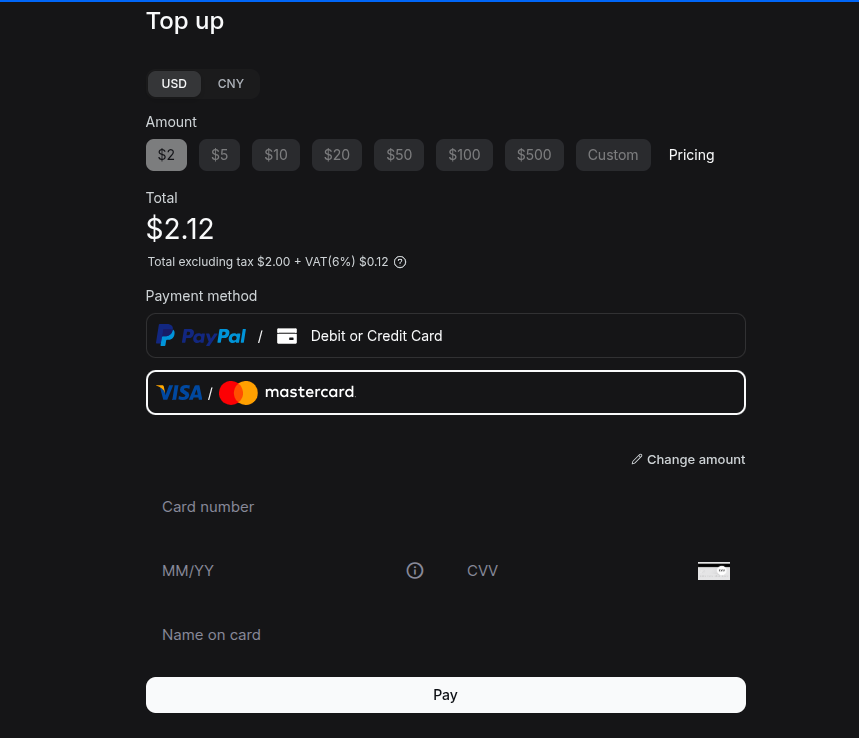

Step 6: Enter your card details and pay. Choose the card payment option, enter the virtual card’s number, expiry, CVV, and the exact billing address from the card app (mismatched addresses are a common silent decline). Confirm. Your balance appears on the Billing page immediately.

That’s it. Your API keys now draw from a funded USD balance, and your local bank’s FX policy is no longer part of your stack.

Why Is My DeepSeek Payment Failing?

Most DeepSeek payment failures originate from issuer-side restrictions, not from DeepSeek itself. Match your error to the table:

| Error / symptom | Likely cause | Fix |

|---|---|---|

| “Do Not Honor” | Your bank is blocking international/FX transactions on this card | Use a USD-denominated card; or call your bank to enable international payments (where policy allows) |

| “Transaction Not Permitted” | Card not enabled for international e-commerce (common default in RW, UG, XOF zone) | Request enablement via your bank, or skip it with a virtual USD card |

| Insufficient FX limit | You’ve exhausted a monthly/quarterly international cap (NG, EG, GH) | Check remaining limit; move recurring foreign payments to a USD card to stop competing with yourself |

| 3D Secure fails to load or verify | Issuer’s 3DS service doesn’t play well with the gateway | Retry once; if persistent, the issuer-gateway pairing is the problem, change the card, not the browser |

| OTP never arrives | Bank’s international OTP delivery is unreliable | Confirm your number with the bank; virtual cards typically verify in-app instead |

| Billing address mismatch | You entered your home address instead of the card’s registered address | Always use the billing address shown in your card app |

| PayPal “can’t complete this transaction” | Your country’s PayPal account is receive-only or send-restricted | PayPal won’t work from that account, use a card instead |

| Card worked before, fails now | Temporary merchant block or a quietly changed bank limit | Wait and retry once; if it recurs, treat the local card as unreliable for this merchant |

One habit that saves pain: test with the smallest top-up first. A $5 success tells you the whole rail works before you commit a larger amount.

Frequently Asked Questions

Can I pay for DeepSeek with a Naira card?

Sometimes. Several Nigerian banks re-enabled international payments on naira cards in 2025 with quarterly limits that vary by bank and continue to change. Success is inconsistent, and the limits are shared across all your foreign spending. A virtual dollar card funded with NGN is the reliable alternative.

Does DeepSeek accept crypto?

No. DeepSeek accepts only card, PayPal, Alipay, and WeChat Pay. You cannot send USDT, BTC, or any cryptocurrency to DeepSeek directly. Stablecoins work only as a funding source; load them onto a virtual dollar card, then pay with the card.

Does DeepSeek accept PayPal?

Yes, DeepSeek accepts PayPal at checkout. The catch is on your side: PayPal accounts in Kenya, South Africa, and Botswana can send payments, while accounts in Nigeria, Cameroon, and several other African countries are restricted. If your PayPal account can’t make purchases, use a card instead.

Is DeepSeek free in Africa?

DeepSeek Chat is free everywhere, including all African countries; no subscription is required. The DeepSeek API is paid and billed in USD per token used. New developer accounts also receive a free grant of around 5 million tokens before any payment is needed.

What is the minimum DeepSeek top-up?

DeepSeek lets you choose preset amounts or enter a custom amount, and small top-ups in the $2–$10 range are accepted. At current V4 Flash pricing, even $5 covers millions of tokens, so starting small is a sensible way to test that your payment method works.

Does DeepSeek balance expire?

No. According to DeepSeek’s official billing FAQ, topped-up balances do not expire. You can fund your account once and draw it down over months, which makes slightly over-funding a safe strategy if cross-border payments are a hassle in your country.

Can I pay for DeepSeek with M-Pesa?

Not directly, DeepSeek has no mobile money option. But M-Pesa is the best funding rail in Kenya and Tanzania: load a virtual dollar card with M-Pesa, then use that card on DeepSeek’s top-up page. The whole flow takes a few minutes from your phone.

Why is my card declined on DeepSeek?

Usually because your bank restricts international or foreign-currency transactions, through FX controls, spending caps, or fraud scoring of unfamiliar gateways, not because of anything on DeepSeek’s side. Check the troubleshooting table above to match your exact error to its cause and fix.

Which African countries can pay for DeepSeek?

All of them, with the right method. Local cards work inconsistently in Nigeria, Ghana, Kenya, and South Africa, and barely at all in Egypt, Malawi, and the XOF/XAF zones. A virtual dollar card funded in local currency or stablecoins works from every African country covered in this guide.

Can I use USDT to pay for DeepSeek?

Not directly, since DeepSeek doesn’t accept crypto. But USDT is an excellent funding source: convert it to the balance of a virtual dollar card, and pay DeepSeek with the card. This is the standard route for freelancers paid in stablecoins and users in parallel-rate economies.

The Bottom Line

DeepSeek has become one of the most affordable AI platforms available to African developers, startups, and businesses. V4 Flash pricing means the API itself is rarely the budget problem. The payment rail is. Local card restrictions differ from Lagos to Cairo to Dakar, but the pattern is the same everywhere: the bottleneck is your currency’s access to dollars at the moment of checkout.

Move the conversion upstream, and the problem disappears. Whether you fund with naira, shillings, cedis, CFA francs, or USDT, a virtual dollar card turns a USD-billed API into a local-currency expense you control.

If your local card keeps getting declined, create a virtual dollar card with EverTry, fund it in your currency, and complete your DeepSeek top-up in under 15 minutes.

This article is provided for informational purposes only and does not constitute financial, legal, tax, investment, or regulatory advice. Payment methods, pricing, platform features, foreign exchange regulations, and bank policies may change without notice and may vary by country, bank, or payment provider. Readers should verify current requirements directly with DeepSeek, their financial institution, and relevant regulatory authorities before making any payment decisions. EverTry does not control, operate, or guarantee the availability of third-party platforms, payment gateways, or services referenced in this article.

Matt Aluya is the founder of EverTry. A software engineer focused on virtual card issuance and stablecoin settlement for cross-border payments in emerging markets. LinkedIn · matt.aluya@evertry.co